What? Where's the Excess Mortality in 2020 Life Insurance Claims?

CDC All-Cause Mortality Data Doesn't Seem to Line Up with Death Benefits

Last Sunday I shared an important news story, first published in The Center Square: The CEO of an Indianapolis-based insurance company had announced that the death rate in 2021 was up a stunning 40 percent from pre-pandemic levels among working-age people, and that most of the excess deaths were not caused by Covid-19.[1]

The story got picked up that same evening by Dr. Robert Malone and then the next morning by Steve Kirsch, both of whom wrote about it on their Substack pages. Kirsch signaled his intent to dig deeper into what he and others surmised might be a potential goldmine of data from life insurance companies about the true impact of the deadly Covid-19 vaccines. Many people consider alternative sources of dependable data essential in light of what is now increasingly understood to be complete corruption at the CDC.

I will leave the analysis of 2021 life insurance data to Kirsch and his team. They can do a much better job with it than I could.

However, the CEO’s comments about 2021 made me curious about the 2020 data. After all, 2020 was the first year of a supposedly worldwide pandemic, one that had led to unprecedented lockdowns, business and school closures, mask mandates and, ultimately, forced vaccination. The CDC told us that Covid-19 had caused hundreds of thousands of deaths in the U.S. and driven all-cause mortality sky high.

So, what does the 2020 life insurance data say about all of this?

What follows may seem a bit tedious, but please stay with me, and hopefully it will be worth your while. I would also like to hear your thoughts.

The first thing I found was a news report announcing that life insurance companies in the U.S. had paid out a record $90 billion in death benefits in 2020. Industry analysts were attributing this 15.4 percent increase in total payments over 2019 directly to Covid-19.[2]

Taken at face value, this report appeared to confirm that the U.S. had indeed suffered a population-wide catastrophe in 2020.

However, a deeper dive into the data revealed a more complex picture.

It turns out that the actual number of life insurance policies paid out in 2020 was unremarkable. In fact, the total number of policies paid out by life insurers in the United States was higher in 2018 than 2020. The number of policies paid out was also higher in 2012 than 2020.

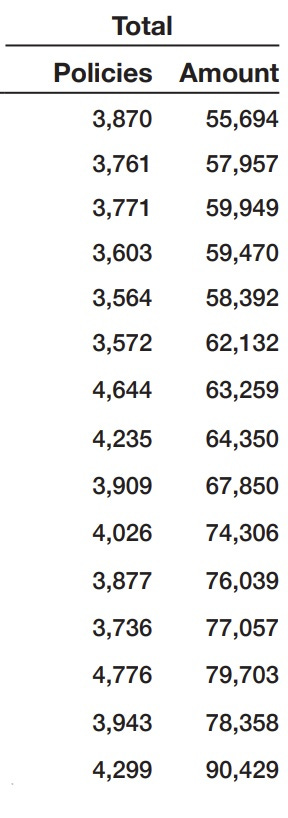

According to the American Council of Life Insurers Life Insurance Fact Book, Chapter 5, Table 5.8, insurers paid out a total of 4,299,000 life insurance policies in 2020, compared to 4,776,000 in 2018 and 4,644,000 in 2012.[3]

The claims data show that the raw number of life insurance policies paid out in 2020 was comparable to that of recent years but that the individual policies were worth more, on average, in 2020 than they had been in previous years.

See Image Below, Excerpted from Table 5 in the Life Insurance Fact Book

The first column shows the number of policies paid out, in the thousands. The second column shows the total amount paid out, in the millions, beginning in 2006 and ending in 2020.

What could explain this? I don’t know. Perhaps because of Covid-19 the U.S. experienced a higher concentration of deaths in wealthier communities, such as nursing homes in New York City. Elderly people in wealthy communities would tend to own more generous insurance policies.

In any case, the data show that the significant increase in the total paid out in 2020 was not the result of an avalanche of excess death claims from Covid or any other cause.

Furthermore, during a cursory review of 2020 quarterly reports from life insurance companies, I was able to quickly identify at least two major insurers – Prudential and Lincoln Financial – that reported paying out a smaller total of death benefits in 2020 than in 2019. So, even the tendency for individual claims to be worth more during Year One of the pandemic did not appear to be industrywide.[4] [5]

So, what exactly can the life insurance data tell us about mortality?

First, since nearly half of Americans have no life insurance, many people who die are never reflected in the insurance claims data. This includes all children.

Despite this fact, the number of policies paid out per year can exceed the total number of people who die. This is because people who carry life insurance often own more than one policy.

For these reasons, it seems the number of insurance policies paid out in any given year can only reveal trends. It cannot be used to ascertain the actual number of people who died that year. Furthermore, the number of policies paid out may be influenced by many factors other than the raw total of all-cause deaths. Risk factors for death may affect different age and economic groups differently, which in turn may affect the likelihood that those who die are carrying life insurance. Regional differences also come into play.

Still, one generally would expect the total number of life insurance policies paid out during a pandemic year to be significantly higher than normal.

The information that would be most valuable for our purposes – the total number of people who hold life insurance, the percentage of policyholders who died, and a breakdown by cause of death -- does not appear to be published by the industry. Extrapolating this information likely would require access to the claims data from individual companies.

Motive, Means, and Opportunity

Thus, with seemingly little more to gain from going further down the life insurance rabbit hole myself, I turned my attention back to the CDC’s Covid and all-cause mortality data from 2020. Like other curious Americans, I had been tracking the CDC’s mortality data closely in 2020. Reports had circulated throughout the year that many deaths from other causes – including, incredibly enough, car crashes – were being misclassified as Covid 19 deaths. Apparently, the federal government offered hospitals strong financial incentives to label every death a Covid death, as Dr. Malone and others have recently explained.

At the same time, lots of videos were circulating online during 2020 of deserted hospital corridors and waiting rooms. TikTok videos of nurses dancing in empty ERs and ICUs because they had no patients to care for suggested that, at least outside the so-called Covid-19 hotspots, critical care was not being stretched thin by Covid or any other illness.[6]

Time would tell. If deaths from other causes were being falsely attributed to Covid, it would have the effect of exaggerating the overall impact of the virus on the population. Fortunately, the all-cause mortality data at the end of the year would clear things up, or so we assumed. Deaths misclassified as Covid could not cause a large swell in overall mortality. They would simply shift the number of dead from other categories to Covid.

Some researchers who were tracking these trends closely said that this is precisely what appeared to be happening.[7] Naturally, their voices were quickly censored.[8] Adding to the controversy was the fact that the CDC, unlike its far superior data management counterpart, the National Health Service in the U.K., apparently has such difficulty trying to count dead bodies in real time that it must continually massage and backfill the data.

For example, an article published in the Journal of the American Medical Association (JAMA) in October 2020 listed the total U.S. deaths from all causes for the period of March 1 – July 31, 2020, as 1,336,561. The final tally for that period, as reported by the CDC in March 2021, was 1,402,000. This means that, sometime after September 2020, the CDC backfilled 65,439 deaths for a period that had ended in July.[9]

While establishing the exact cause of death in each case understandably takes time, what could be so difficult about merely counting and reporting to a central database the number of people in your community declared dead each day?

Just like national elections that now last an entire month instead of a single day, allowing continual backfill and tweaking of such politically charged public health tracking systems as all-cause mortality would seem to invite abuse. What’s to stop scheming politicians from conspiring with corrupt government bureaucrats to manipulate the data in favor of a desired outcome?

But what would be the motive for manipulating death data in 2020? Well, we know that throughout 2020 the CDC was eagerly anticipating the development and authorization of a brand-new Covid-19 vaccine. As RFK Jr.’s blockbuster must-read book, The Real Anthony Fauci, meticulously lays out, the agency has evolved into little more than a front group for the pharmaceutical industry. It now exists primarily to sell vaccines. Officials at the CDC had a strong motivation to create maximum demand for their new experimental vaccine by every means possible, including potentially inflating death statistics.

I am not saying that the CDC manipulated the 2020 all-cause data. I am only saying that the agency clearly had the motive, means and opportunity to do so.

Without independent confirmation from a non-compromised source, all I can report for certain is this: After it finished massaging and backfilling the data, the CDC released a final death toll for 2020 of 3,358,814, of which 351,655 deaths were attributed to Covid-19. The total all-cause number, in absolute terms, was approximately 15 percent higher in 2020 relative to 2019. Mortality not attributed to the virus was up 5 percent over 2019. That’s more than 150,000 EXCESS deaths from causes other than Covid. This by itself was highly unusual. The annual increase in all-cause mortality had averaged 1.6 percent from 2013 to 2019.

Researchers have struggled to explain this non-Covid excess mortality in the U.S., which started in March 2020, almost precisely from the moment that the World Health Organization declared Covid-19 a pandemic, and even before the Trump Administration announced its “two weeks to flatten the curve” social-distancing strategy.

According to another report in JAMA, between March 1, 2020, and April 25, 2020, 87,001 excess deaths were recorded in the U.S., of which 35 percent were unrelated to Covid. Large increases in mortality were observed from heart disease, diabetes, and numerous other diseases. In 14 states, including California and Texas, more than 50 percent of EXCESS deaths were attributed to causes other than Covid. The five states with the most Covid deaths also reported large increases in deaths from diabetes, heart disease, Alzheimer’s, and cerebrovascular diseases. New York City recorded the largest increases in non-respiratory deaths, most notably from heart disease and diabetes.[10]

By stark contrast, large increases in non-respiratory, non-Covid deaths did not occur in all parts of the U.S. Nor did they occur in Canada or Western Europe,[11] even though their populations suffered the same brutal shutdowns, lockdowns, and scare tactics as we did.

If the lockdowns led to premature death from sedentary lifestyles and/or delayed medical treatment, then why is excess mortality from a variety of diseases observed right from the start of the WHO-declared pandemic? Why did all states and nations that suffered the same pandemic and lockdowns not experience these non-Covid excess deaths? And, if deaths were up by more than 15 percent in 2020 relative to 2018, why were more life insurance policies paid out in 2018?

Once again, I’m not saying that either the Covid or the all-cause mortality data was falsified. Astute readers are surely wondering why the CDC would even think to inflate non-Covid deaths as a way to sell its Covid vaccines? I don’t have the answer, but if deaths from other causes were being moved into the “Covid” column throughout the year, those who were doing the manipulating may have felt uneasy about how it would all look in the end. In that case, simply inflating deaths from all causes might have seemed the safest bet. Or perhaps they were merely aiming to create a picture of maximum damage to overall health from the pandemic, thus setting the stage for the vaccine to swoop in and save the day.

Why Does Any of This Matter?

Some may ask, what’s the point of going back to 2020? Shouldn’t we focus our attention on 2021 and beyond.

The point is that the closer we look at each year of the pandemic, the more apparent it becomes that we no longer have a trustworthy, independent, non-compromised source of something so vitally important as death statistics in the U.S. Going forward we are going to need to find a reliable way to count deaths -- from the virus, the vaccine, and all other causes.

The reason Malone, Kirsch, and others are now interested in analyzing private insurance data is because they no longer trust the CDC, and for good reason. We have watched the agency under both Trump and Biden lie to us about literally everything – case counts, PCR tests, lockdowns, masks, vaccine dangers, vaccine failures. Why wouldn’t the agency lie to us about deaths? In 2020 the CDC had an experimental vaccine to sell. In 2021-22 it has a deadly vaccine to cover up.

Life insurance data may serve as a check on some CDC corruption, but it will never be an adequate substitute for an honest, competent federal health agency. Most importantly for writers like me, since children don’t carry life insurance, it will never be able to tell us anything about children.

What do you think? Should we take the CDC death statistics at face value? If not, what should be our truth-seeking strategy going forward?

Please post your comments below the references. Then share this report with whoever you think may be interested. Thank you!

[1] Insurance CEO Says Deaths Way Up, Not from Covid (substack.com)

[2] Life insurance payouts spiked in 2020 — largest rise since 1918 flu pandemic (nypost.com)

[3] 05fb21_chapter5_expenditures.pdf (acli.com)

[4] Exhibit 99.2 - 4Q20 QFS (q4cdn.com) pp. 20 and 21

[5] 4Q2020 LNC Statistical Supplement - Copy.xlsx (lfg.com) p. 19

[6] Tik Tok Dancing Nurses? What Is This Garbage? Empty Hospitals? - YouTube

[8] A closer look at U.S. deaths due to COVID-19 - The Johns Hopkins News-Letter (jhunewsletter.com)

[9] Excess Deaths From COVID-19 and Other Causes, March-July 2020 | Cardiology | JAMA | JAMA Network

[10] Excess Deaths From COVID-19 and Other Causes, March-April 2020 | Population Health | JAMA | JAMA Network

[11] 1635189453861_USA ACM into 2021 - article----12d.pdf (denisrancourt.ca)

I think that the insurance data RIGHT NOW would be valuable to have, but I think the moment that report (The original that brought it to attention) was released, I think they (they being insurance companies under pressure politically) would have started laying the ground work for obscuring it. They'll have added policy changes, rules etc to allow for non-transparency.

Lawyers with FOI requests now would be a good idea, if it's not already too late to snap shot the data from 2015-2021.

There is a lot of what seems to be missing and what needs to be honestly and transparently analyzed. It is possible that Covid causes delayed deaths, in addition to vaccines causing immediate deaths (1-2 weeks after injections) and delayed deaths as well.

I am not holding my breath,m but in a good country deaths would be released along with some demographic information like "64 year old female, resident of Owasso OK, died on Nov 16, 2020", with perhaps some info from death cert.